What is the Asset Dedication Strategy?

How does the Asset Dedication Strategy work?

Step 1: Secure future cash flow needs

Whether a client is saving for a down payment on their first home, preparing for their first years of retirement or looking to protect their principal for another cash flow need, they should have investments that can help them fulfill those needs regardless of how the market reacts. Given this, we purchase fixed income securities to generate the specific cash flows when they need them. Learn More…

Predictable Cash Flows

Principal Protection

Rising Rate Risk Reduction

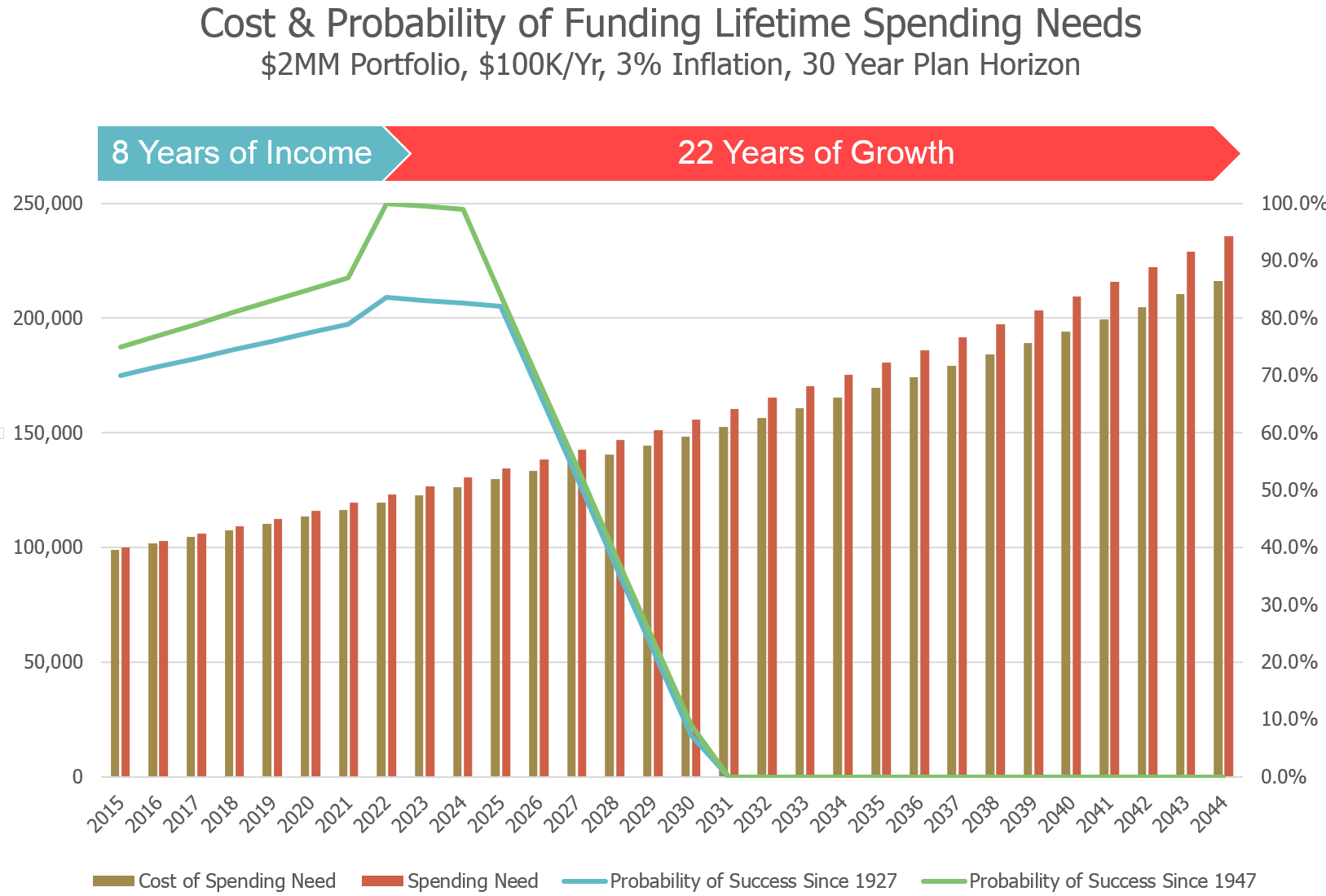

For clients in retirement, we look at their projected lifetime spending needs and current account balances to back into a portfolio that has been historically sustainable. By approaching the composition of the portfolio with this liability-driven approach, we seek to better balance the risk and return profile in the context of the clients future financial goals. In the example below, we found that the client would be best served by an income portfolio that was able to fund the first 8 years of their spending needs.

Determine the Initial Allocation

Monitor and Adjust as Needed

For clients nearing retirement, we look at their projected lifetime spending needs and current account balances to find out how many years of retirement income they should purchase initially and how much they should contribute in remaining years leading up to retirement so that they have a portfolio that has been historically sustainable. By approaching the composition of the portfolio with this liability-driven approach, we seek to better balance the risk and return profile in the context of the clients future financial goals.

In the example below, we found that the client would be best served by an income portfolio that was able to fund the first 8 years of their spending needs.

For clients in the accumulation stage, we first seek to better balance the risk and return profile of the goals with shorter time-horizons (ex. college) and then invest the remainder in combinations of asset classes that have historically maximized minimum and average returns over longer time horizons.

If a client is weary of having a larger allocation to equities, we can invest the principal that the investor wants to protect in investment grade securities that are at advantageous points along the yield curve. Doing so, they can earn a higher return than cash and better protect their investments from rising interest rates than if they invested in bond funds.

Step 2: Align growth investments with time-based goals

Over and over again, the market has showed us that the longer you stayed invested in equities, the better chance you have of seeing higher returns. However, most investors cannot afford to leave their equity investments in the market forever. Given these realities, we built growth portfolios that use game theory algorithms that seek to improve a client’s probability of reaching a time-based goal by maximizing minimum returns. Learn More…

Mitigation of time-based risks

Risk-aligned diversification

Maximized minimum returns

Step 3: Monitor and adjust to build a portfolio that lasts a lifetime

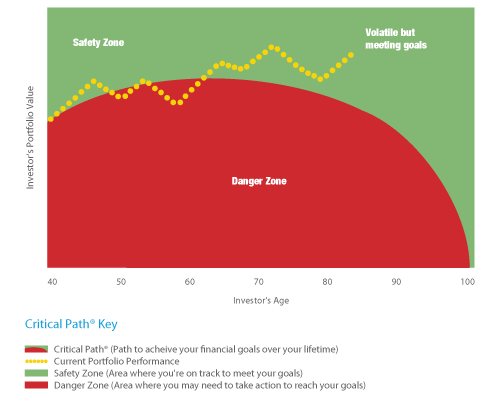

As time goes on, most clients contemplate adjusting their financial plans but are unsure as to how the adjustments will impact their chances of reaching the long-term goals. Given this, we created a decision making framework and reporting system (the Critical Path) that intuitively reflects the progress an investor’s defined income portfolio and growth portfolio are making towards the goals laid out in their financial plan and what certain adjustments will do to their probabilities of success during every rolling period dating back to the Great Depression. Click here to learn more…

- Probability of Success in 1932 85%

- Probability of Success in 1974 95%

Meet with a Team Member

Fill out the form below, and you will be directed to our online meeting scheduler.